By Stephanie Bryant-Erdmann, USW Market Analyst

With wheat harvest underway in the Northern Hemisphere and wheat planting underway or complete in the Southern Hemisphere, wheat buyers are beginning to see a downward trend in production numbers. As discussed in the June 15 Wheat Letter, the high quality, high protein wheat supply is shrinking and supporting prices. USDA expects global output to decrease for the first time in five years to 739 million metric tons (MMT) (27.2 billion bushels), down 14.6 MMT (535 million bushels) from the 2016/17 record of 754 MMT (27.7 billion bushels). If realized, production would be 3 percent above the five-year average. In this issue, we summarize current expectations and conditions in the world’s major wheat exporting countries, which account for 90 percent of all world wheat exports.

Argentina. In June, Bolsa de Cereales, the Buenos Aires Grain Exchange, reported Argentine farmers will plant 17 percent more wheat acres in 2017/18 as wheat production continues to expand under President Macri’s favorable policies. Bolsa estimated wheat planted area at 13.6 million acres (5.5 million hectares). On June 22, 53 percent was planted, up from 37 percent the prior week. USDA’s July estimate for 2017/18 Argentinian wheat production was 17.5 MMT (643 million bushels), up 3 percent from 2016/17 and 41 percent greater than the five-year average.

Australia. In its June report, the Australian Bureau of Agricultural and Resource Economics and Science (ABARES) forecasted 2017/18 production at 24.2 MMT (889 million bushels). That is 31 percent below 2016/17, due to an expected 25 percent reduction in average yield and a slight decline in planted area from 2016 to 31.4 million acres (12.7 million hectares). Autumn rainfall was below normal in Western Australia and variable across South Australia, states that account for roughly half of Australia’s winter crop planted acres and production. The Australian Bureau of Meteorology expects drier than average conditions across wheat producing regions during the next three months.

Black Sea. Winter wheat harvest is underway and USDA projects combined 2017/18 output from Russia, Ukraine and Kazakhstan will decrease 6 percent to 107 MMT (3.93 billion bushels) based on an expected return to trendline yields. If realized, the combined harvest would still be greater than the five-year average. Russian consultancy SovEcon pegged Russian planted wheat area at 68.9 million acres (27.9 million hectares), down slightly from 2016/17 due to a 4 percent decrease in spring wheat area. Russian wheat production is expected to decline to 70.4 MMT (2.59 billion bushels), down 3 percent from 2016/17 due to the smaller planted area and anticipated lower yields. SovEcon forecast Russian winter wheat yields at 52.1 bu/acre (3.50 MT/ha), down from 55.5 bu/acre (3.73 MT/ha) in 2016/17. Spring wheat yields are expected to fall 7 percent year over year to 21.1 bu/acre (1.42 MT/ha). UkrAgroConsult reported Ukrainian wheat planted area decreased slightly year over year to 15.6 million acres (6.30 million hectares), and expects yields to fall 7 percent year over year to 58.2 bu/acre (3.91 MT/ha). 2017/18 Ukrainian wheat production is forecast at 24.5 MMT (900 million bushels), compared to 26.1 MMT (959 million bushels) in 2016/17. UkrAgroConsult noted yield declines and a 3 percent smaller planted area will lower Kazakhstan wheat production to 13.7 MMT (503 million bushels), down 9 percent from 2016/17, if realized.

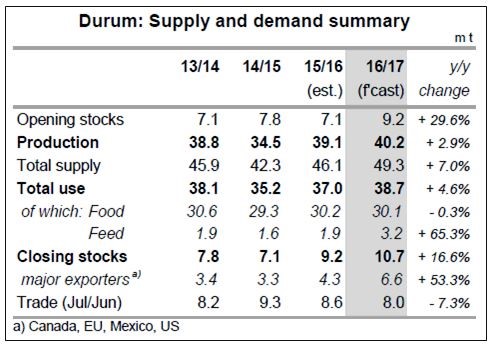

Canada. Agriculture and Agri-Food Canada (AAFC) expects wheat production of 29.5 MMT (1.08 billion bushels) in 2017/18. That is down 7 percent year over year because average yield is expected to decline to 47.6 bu/acre (3.20 MT/ha) in 2017/18. Slightly higher planted area will partially offset expected yield declines. StatsCan put planted area at 22.4 million acres (9.07 million hectares) of wheat in 2017/18. Spring wheat planted area rose 2 percent to 15.8 million acres (6.39 million hectares) due to low carry-in stocks and increased price competitiveness with alternative crops. Durum planted area decreased 16 percent year over year to 5.2 million acres (2.11 million hectares) due to high carry-in stocks and lower prices. Canada’s winter wheat seeding decreased 16 percent year over year from a shift to spring wheat. Crop conditions this year are variable with excessive moisture in northern areas while southern areas remain dry. As of June 23, topsoil moisture in Saskatchewan was rated 18 percent short or very short compared to 40 percent short or very short last week. In Alberta, 84 percent of spring wheat is rated in good to excellent condition compared to 83 percent last year. Surface soil moisture is rated 79 percent good to excellent; 14 percent of surface soil moisture is rated excessive. Saskatchewan and Alberta account for roughly 82 percent of 2017/18 planted wheat acres.

European Union. After a challenging 2016/17, Strategie Grains expects EU common wheat production will rebound 4 percent to 142 MMT (5.20 billion bushels) in 2017/18 with a 5 percent increase in yield expected to offset a 1 percent decrease in planted area. French production is expected to increase 7.66 MMT (281 million bushels) year over year to 35.6 MMT (1.31 billion bushels) — a 33 percent improvement in yields. Precipitation across France is 25 percent below normal since March, however. The French crop bureau FranceAgriMer rated 68 percent of French soft wheat in good or excellent condition, down from 74 good to excellent percent the prior week. Dry conditions are also threatening yield potential in Austria, Germany, Italy and Poland. In Spain, drought conditions are expected to cut wheat production by 32 percent year over year to 4.72 MMT (173 million bushels). Additionally, the EU’s crop monitoring service MARS reduced its forecasts for wheat yields to 87.2 bu/acre (5.86 MT/ha), from 87.9 bu/acre (5.91 MT/ha) in May, but greater than the five-year average of 86.7 bu/acre (5.84 MT/ha). Weather forecasts for early July provide little relief for EU farmers, which could further threaten yield potential.

United States. USDA forecast U.S. 2017/18 wheat production at 49.6 MMT (1.82 billion bushels), down 21 percent year over year and 15 percent below the five-year average due to an anticipated 10 percent decline in average yield and the lowest number of planted acres since USDA records began in 1919. USDA expects the average yield to be (3.18 MT/ha) compared to the five-year average of (3.14 MT/ha). In the March 31 Prospective Plantings report, USDA reported U.S. farmers intended to plant 46.1 million acres (18.7 million hectares) of wheat for 2017/18.

USDA will update planted area estimates June 30. The first U.S. by-class estimates will be released in the July 12 World Agricultural Supply and Demand Estimates (WASDE) report.

Follow #wheatharvest17 on Twitter for the latest harvest photos and conditions.

Subscribe to USW Weekly Harvest Reports. To read the latest report, click here.