By Claire Hutchins, USW Market Analyst

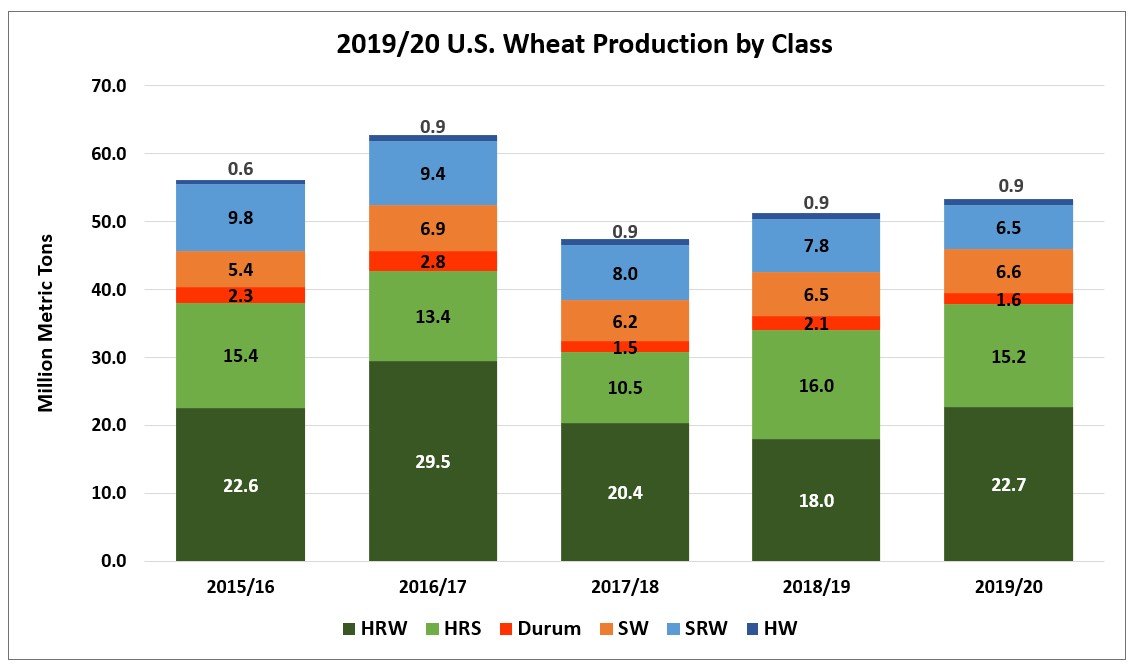

On Sept. 30, USDA released its Small Grains Summary noting that 2019/20 U.S. wheat production increased to 53.3 million metric tons (MMT), up 4 percent from last year due to significant improvements in yield despite lower planted area. While this is still 2 percent below the 5-year average of 54.2 MMT, the production volume coupled with significant carry-in stocks ensure that the U.S. wheat remains the most reliable supply for 2019/20. Here is a look at 2019/20 U.S. wheat production by class.

USDA’s Small Grains Summary indicates U.S. wheat yields offset a reduced planted area for 2019/20.

Hard Red Winter (HRW). Last fall, U.S. farmers decreased HRW planting in the U.S. Southern and Central Plans due to extremely wet conditions which delayed the soybean harvest and in turn HRW planting. A slight uptick in planted area in Montana and South Dakota partially offset reductions in other states. Total U.S. HRW planted area fell 2 percent year-over-year to 22.7 million acres (9.19 million hectares), 15 percent below the 5-year average of 26.6 million acres (10.8 million hectares). Cool temperatures and favorable moisture during the growing season boosted HRW yields substantially year-over-year in Kansas, Nebraska and Oklahoma. In Kansas, the largest HRW producing state, a higher average yield offset lower planted area and production increased 22 percent over 2018/19 levels to 338 million bushels (9.17 MMT). USDA estimates total 2019/20 HRW production increased 26 percent over last year to 834 million bushels (22.7 MMT).

Hard Red Spring (HRS). Cold soil temperatures and excessive moisture in certain areas delayed HRS planting across much of the Northern Plains. USDA says U.S. farmers planted 12.0 million acres (4.86 million hectares), 6% below last year but slightly higher than the 5-year average of 11.8 million acres (4.78 million hectares). A cool summer boosted HRS yields in Montana and South Dakota. Heavy, persistent rain has severely delayed the 2019 HRS harvest. According to USDA, as of September 30, U.S. spring wheat harvest is only 90 percent complete compared to the 5-year average of 99 percent. USDA estimates 2019 HRS production will total 558 million bushels (15.2 MMT), 5 percent lower than 2018, but 8 percent higher than the 5-year average of 518 million bushels (14.1 MMT).

Soft Red Winter (SRW). Last fall, U.S. farmers planted 5.54 million acres (2.24 million hectares) of SRW, down 6 percent from the year prior and 18 percent from the 5-year average of 6.7 million acres (2.71 million hectares) due to low wheat prices compared to soybeans and delayed planting. Excessive moisture continued through the growing season and slowed harvest progress in many places. USDA reported SRW production totaled 239 million bushels (6.50 MMT), down 16 percent from last year and 31 percent below the 5-year average of 348 million bushels (9.46 MMT).

White Wheat (Soft White, Club and Hard White). U.S. white wheat planted area fell 4 percent below 2018/19 levels to 3.95 million acres (1.60 million hectares). Mild growing conditions and good soil moisture in the Pacific Northwest (PNW) supported above-average winter and spring wheat yields. The average white winter wheat yield in Oregon increased 1.0 bu/acre (.067 MT/hectare) over last year to 68.0 bu/acre (4.57 MT/hectare) in 2019. Slightly lower planted area and above-average yields kept U.S. white wheat production stable year-over-year at 273 million bushels (7.43 MMT) and 8 percent higher than the 5-year average of 252 million bushels (6.87 MMT).

Durum. Anticipating less-than break even prices, farmers planted less durum area this year. In its Small Grains 2019 Summary, USDA estimated 1.34 million acres (542,000 hectares) were planted to durum, down 35 percent from 2018/19 and 32 percent below the 5-year average of 2.0 million acres (664,000 hectares). USDA estimated total 2019/20 U.S. durum production at 57.3 million bushels (1.57 MMT), down 26 percent from last year. Cool, wet weather boosted yields in the U.S. Northern plains. Both Montana and North Dakota durum yield potential reached a record high in 2019. The country’s average durum yield also reached a record high of 44.8 bu/acre (3.01 MT/hectare), up 13 percent from last year. However, as with HRS, a significant portion of the northern durum crop has not yet been harvested. Desert Durum® production fell 46 percent year-over year to 5.67 million bushels (154,000 MT) due to sharply lower planted area in both Arizona and California.