U.S. Wheat Export Basis to Remain High Until March 2021

By Claire Hutchins, USW Market Analyst

Since June, U.S. Wheat Associates (USW) has carefully tracked the relationship between limited export elevation capacity and high U.S. wheat export basis values. Significantly greater Chinese demand for U.S. agricultural products has limited export elevation availability, causing an increase in wheat export basis values for October 2020 through February 2021 deliveries. However, the anticipation of seasonally reduced Chinese demand for U.S. agricultural goods could pressure U.S. wheat export basis levels for March 2021 and forward delivery periods.

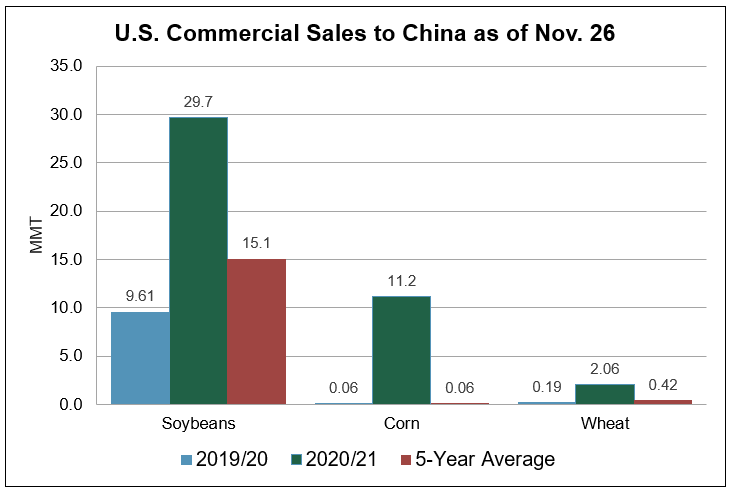

The United States has sold historic levels of soybeans, corn and wheat to China for delivery in 2020/21 following the Phase 1 Trade agreement between both countries. As of Nov. 26, soybean sales to China at 29.7 million metric tons (MMT) are more than three times greater than this time last year and are nearly double the 5-year average. Corn sales to China at 11.2 MMT are magnitudes greater than late November last year and the 5-year average. Total wheat sales to China at 2.06 MMT are more than ten times greater than this time last year and are nearly five times greater than the 5-year average.

Source: USDA FAS Commercial Sales data

“January, February and the beginning of March are at capacity; we can’t add a lot more business for those months,” said one industry contact. “If anyone were to sell anything for those delivery periods, it would raise elevation costs substantially more.”

Though wheat export basis levels are projected to remain high through early March 2021 as traders work to execute the large volume of existing commodity sales, industry contacts currently predict a sizeable decrease in U.S. wheat forward export basis values if China’s demand for U.S. corn subsides and if Chinese buyers shift to importing Brazilian soybeans.

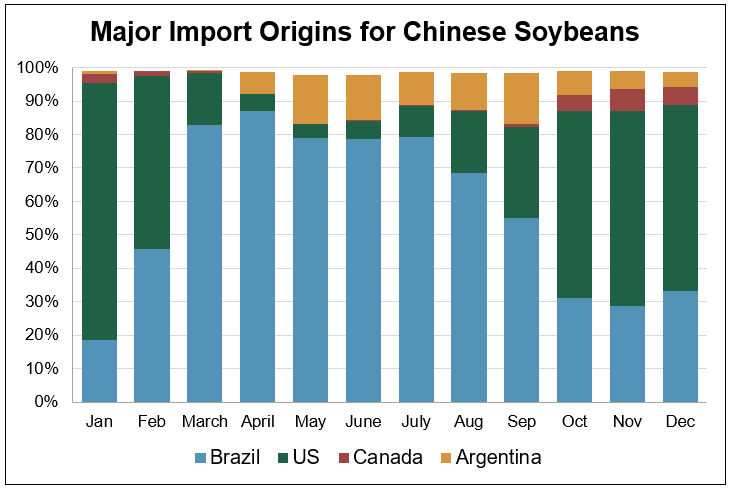

According to Trade Data Monitor (TDM), most Chinese soybean imports usually come from the United States between October and February and from Brazil between March and September. On average, soybeans from Brazil jump from 46 to 83 percent of China’s total imports between February and March. Traders anticipate this seasonal trend will continue in 2021, which could increase U.S. wheat export elevation availability in the Pacific Northwest (PNW) and Gulf and could decrease wheat export basis levels from those regions.

Source: Trade Data Monitor, Chinese soybean import data from 2015 to 2019

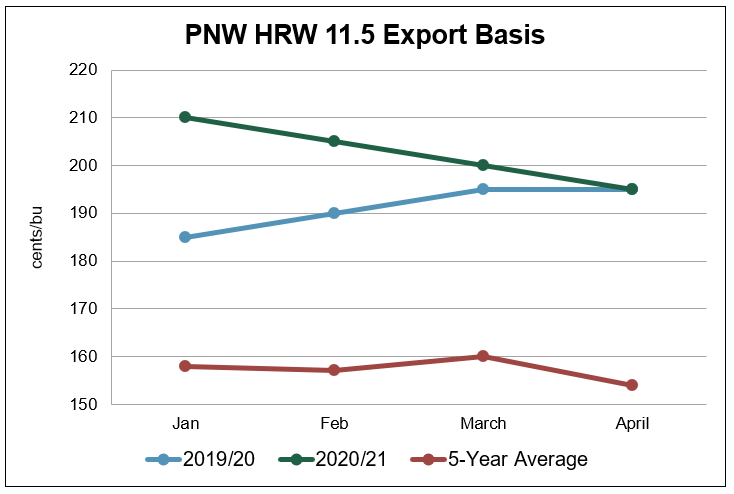

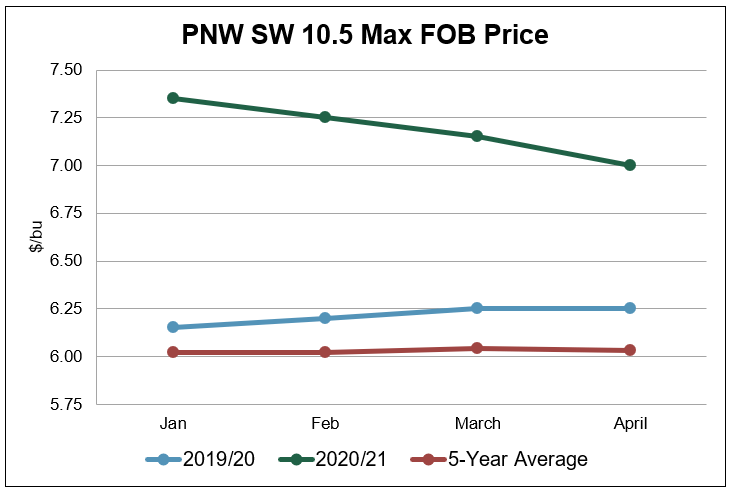

The latest USW Price Report indicates the trade has assumed Chinese demand will slow in the first three months of 2021. The current export basis delivery values for PNW hard red winter (HRW) 11.5 protein show a 5 percent inverse between February and April deliveries.

Source: USW Price Report data as of Dec. 4

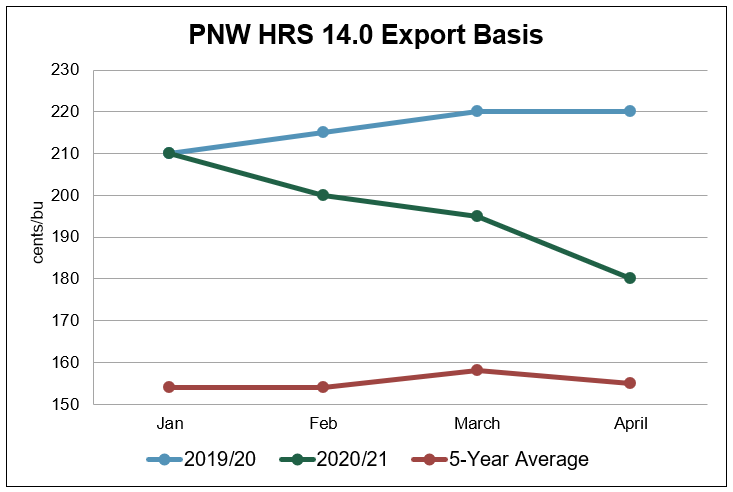

The report also shows a 10 percent inverse between February and April export basis levels for PNW hard red spring (HRS) 14.0 percent protein.

“April forward is when export basis really lightens up and we become more competitive,” said one trader, “there’s strong interest in U.S. spring wheat for that period.”

Source: USW Price Report data as of Dec. 4

While Gulf HRW and soft red winter (SRW) export basis values are forecast to remain relatively stable over the first few months of 2021, the Gulf HRS 14.0 percent protein export basis forecast currently shows a 16 percent inverse between February and April deliveries.

Source: USW Price Report data as of Dec. 4

USW does not have a crystal ball, but we do expect downward pressure on most U.S. wheat export basis values between February and April 2021, as long as China’s import demand for U.S. corn and soybeans slows down and inland logistics continue operating smoothly. USW will continue to monitor trade and logistical developments in the coming months and will communicate anticipated basis changes to our customers.