Opportunities Abound for Customers to Lock-in Competitive Prices

By Stephanie Bryant-Erdmann, USW Market Analyst

Sharply lower U.S. wheat production pushed futures prices to 2-and 3-year highs earlier this summer. However, bearish factors have recently pushed prices down. And when wheat futures are under pressure, wheat importers have the opportunity to lock in competitive prices and maybe even find some bargains.

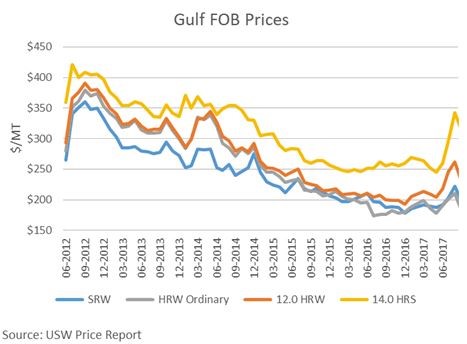

Chicago Board of Trade (CBOT) soft red winter (SRW) wheat futures and export basis are both under pressure from a growing 2017/18 (June to May) supply, which USDA estimated at 14.2 million metric tons (MMT). The year-to-date average SRW Gulf FOB value of $196 per metric ton (MT) is $50 below the 5-year average, and this is a very good quality new crop (for more information on 2017/18 SRW quality, read “Millers and Processors Should Like the 2017/18 Soft Red Winter Crop” below).

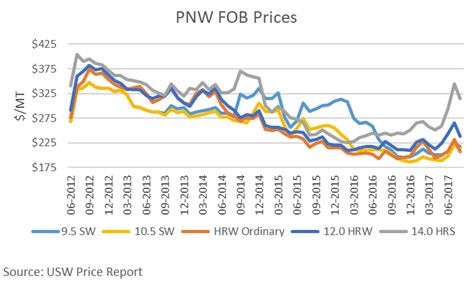

Though U.S. hard red winter (HRW) production is forecast to shrink 30 percent in 2017/18, year-to-date Kansas City Board of Trade (KCBT) HRW wheat futures average $58 per MT below the 5-year average. This is due mainly to KCBT contract specifications and lower average protein levels in the 2016/17 and 2017/18 crops. While HRW futures trickle lower, protein premiums continue to widen. Historically, Gulf HRW protein premiums ranged between $1.50 to $4.40 per MT for each additional 0.5 percent of protein. Pacific Northwest (PNW) HRW protein premiums normally average $2.95 to $7.35 per MT. In 2017/18, that range is now $11 to $32 per MT for the Gulf and $8 to $18 per MT for the PNW.

The widening protein premiums represent the tightening global supply of higher protein wheat. Yet FOB prices for 12 percent Gulf and PNW HRW are $40 and $41 per MT below the 5-year averages, respectively (all U.S. wheat protein is based on 12% moisture). Customers who can use lower protein HRW can take advantage of FOB prices for ordinary/unspecified protein HRW, which are $73 per MT below historic levels at the Gulf and $57 per MT below the 5-year average in the PNW. Preliminary data shows 2017/18 HRW average protein is 11.5 percent, slightly above last year’s final of 11.2 percent, but below the 5-year average of 12.6 percent.

The Minneapolis Grain Exchange (MGEX) hard red spring (HRS) wheat futures have retreated from the 3-year highs reached earlier this summer. However, U.S. and Canadian spring wheat production estimates are supportive of current price levels. StatsCan expects Canadian wheat production (excluding durum) to fall 7 percent to 22.3 MMT. MGEX HRS futures are hovering near the August 5-year average of $6.79 per bushel ($249 per MT), but HRS export basis levels are $15 to $25 per MT below normal at both PNW and Gulf export locations. With harvest still underway in the U.S. Northern Plains and Canada, customers can mitigate some of their risk by locking in these competitive basis levels.

Export pricing for soft white (SW) wheat is not tied to a wheat futures market, but as noted in the July 27 Wheat Letter, protein premiums are shrinking for SW due to the excellent quality and more normal protein distributions in recent crops. PNW FOB export prices for 10.5 max protein SW are $62 per MT below the 5-year average, while FOB prices for 9.5 max protein SW are $70 per MT lower.

Well-informed customers can take advantage of these buying opportunities and lock in lower prices for high-quality U.S. wheat in the next few weeks. Your local USW representative is ready to help answer any questions about U.S. wheat pricing or the U.S. wheat marketing system. To track U.S. wheat nearby prices, review and/or subscribe to the USW Price Report here.