U.S. Wheat Associates (USW) works on behalf of U.S. wheat producers to help the world’s wheat buyers, millers, bakers, wheat food processors and government officials understand the quality, value and reliability of all six classes of U.S. wheat.

The U.S. grain marketing system is a consistently reliable and transparent resource, but it can be a bit complicated for new and, sometimes, experienced buyers to navigate. That is why USW focuses so much of its activity on trade service, keeping buyers and processors informed about crop quality and prices, and how to use the grain marketing and inspection system to protect value and better manage price risks.

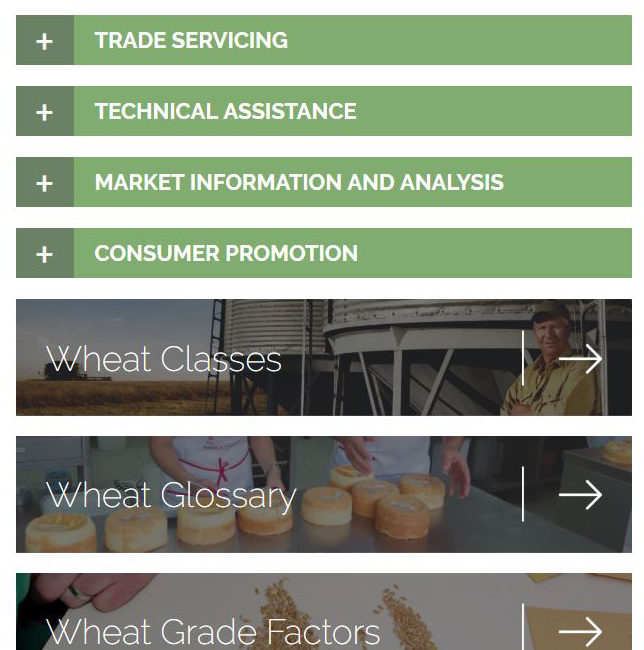

This is a crucial effort giving buyers and users the ability to specify the qualities necessary for almost every end-use product from among the six classes grown across the country. Our dedicated staff is well equipped to help individual customers get the best value possible. They are backed by a wide range of support posted on the USW website at www.uswheat.org. “Working with Buyers” is a very informative section of the site and provides, in effect, a primer on U.S. wheat classes and grade factors, the basic “language” of the U.S. wheat marketing system and other resources available to international wheat buyers.

The opening page of Working with Buyers describes the basic services USW provides, including: trade servicing to answer questions and resolve issues in purchasing, shipping or using U.S. wheat; technical assistance to help strengthen milling, storage, handling and end-product industries; market information and analysis that may affect imports, and projections for future wheat production and consumption; and promotion to expand consumer awareness and appreciation for wheat foods.

All six U.S. wheat classes are profiled next in the section, along with a map showing their general production areas. Milling and processing characteristics and examples of wheat foods made with flour from each class round out this page.

There is a glossary of terms that help the buyer better understand the U.S. grain marketing and grading system. Wheat grades reflect the physical quality and condition of a sample and thus may indicate the general suitability for milling. Terms such as test weight, vitreous kernels and defects are included in this information along with “non-grade” data terms including dockage, protein, ash and kernel size and weight. Representative terms associated with flour and dough performance have their own sections. Baking evaluations, with annual results summarized in the USW Crop Quality reports, are also explained.

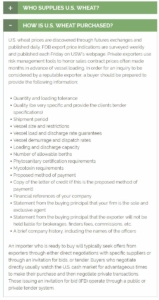

Still another section of this resource pulls together the other information to explain “How to Buy” U.S. wheat. It covers the U.S. wheat supply chain, production and grain shed regions and notes on who supplies wheat, and how it is transported, to the export elevators. Quality assurance through the Federal Grain Inspection Service is detailed along with the contracting process and financial arrangements.

Finally, a Resources section of Working with Buyers includes links to several other relevant materials. Here you can learn how wheat and flour testing is done, how USW collects and analyzes almost 2,000 annual crop quality samples and more.

This combination of reliability and quality provides excellent value to U.S. wheat customers. And the U.S. wheat marketing system can work effectively for buyers and end-product users. When USW representatives are, briefly, not available, we hope you will remember to look online for the Working with Buyers resource.